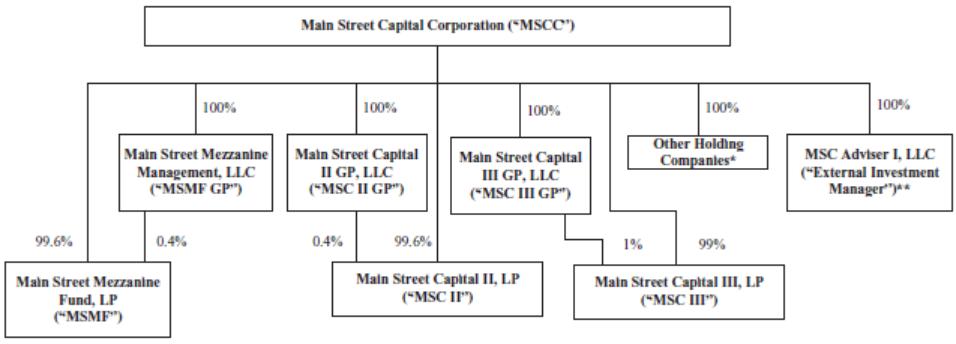

The following diagram depicts our organizational structure:

* | Other Holding Companies includes the Taxable Subsidiaries and other entities formed for operational purposes. Each of these companies is directly or indirectly wholly owned by MSCC. |

** | The External Investment Manager is accounted for as a portfolio investment at fair value, as opposed to a consolidated subsidiary, and is indirectly wholly owned by MSCC. |

CORPORATE INFORMATION

Our principal executive offices are located at 1300 Post Oak Boulevard, 8th Floor, Houston, Texas 77056. We maintain a Web site on the Internet at www.mainstcapital.com. We make available free of charge on our Web site our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and all amendments to those reports as soon as reasonably practicable after such material is electronically filed with or furnished to the SEC. Information contained on our Web site is not incorporated by reference into this Annual Report on Form 10-K, and you should not consider that information to be part of this Annual Report on Form 10-K. Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and all amendments to those reports and other public filings are also available free of charge on the EDGAR Database on the SEC’s Web site at www.sec.gov.

OVERVIEW OF OUR BUSINESS

Our principal investment objective is to maximize our portfolio’s total return by generating current income from our debt investments and capital appreciation from our equity and equity-related investments, including warrants, convertible securities and other rights to acquire equity securities in a portfolio company. Our LMM companies generally have annual revenues between $10 million and $150 million, and our LMM portfolio investments generally range in size from $5 million to $50 million. Our Middle Market investments are made in businesses that are generally larger in size than our LMM portfolio companies, with annual revenues typically between $150 million and $1.5 billion, and our Middle Market investments generally range in size from $3 million to $20 million. Our private loan (“Private Loan”) portfolio investments are primarily debt securities in privately held companies that have been originated through strategic relationships with other investment funds on a collaborative basis, and are often referred to in the debt markets as “club deals.” Private Loan investments are typically similar in size, structure, terms and conditions to investments we hold in our LMM portfolio and Middle Market portfolio.

We seek to fill the financing gap for LMM businesses, which, historically, have had limited access to financing from commercial banks and other traditional sources. The underserved nature of the LMM creates the opportunity for us to meet the financing needs of LMM companies while also negotiating favorable transaction terms and equity participations. Our ability to invest across a company’s capital structure, from secured loans to equity securities, allows

3